Deep-dive AI research reports on individual stocks, powered by our proprietary signals. Every report carries a direction (Bullish or Bearish) and a conviction level(Strong or Speculative). We track stock performance since each report's publication date — because we believe great analysis should be held accountable.

The Kitchen Sink Quarter: Why Molina Healthcare's Panic Sell-Off is a Classic Mispricing

Molina Healthcare's stock plunged after a tough Q4 2025 and weak 2026 guidance. However, the sell-off is a mispricing. Management is taking aggressive, one-time actions to exit a troubled business and reset for a future margin recovery, creating a contrarian opportunity.

The Anatomy of a Mismatch: Why ADMA Biologics' Panic Selloff is a Contrarian Goldmine

ADMA's panic selloff is a contrarian opportunity. The CEO's stock sales and a misunderstood $125M share buyback triggered the crash, but the company's fundamentals remain strong.

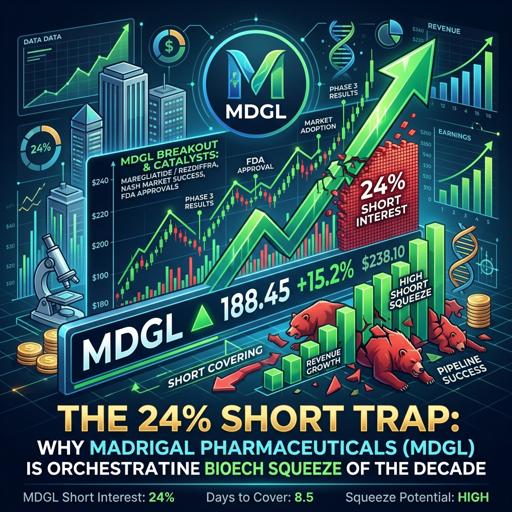

The 24% Short Trap: Why Madrigal Pharmaceuticals (MDGL) is Orchestrating the Biotech Squeeze of the Decade

Madrigal Pharmaceuticals (MDGL) is poised for a major short squeeze. With 24% of shares short, bears are misreading the data. The company has neutralized the GLP-1 threat via a licensing deal, extended key patents to 2045, and is hitting revenue milestones.

The Asymmetric Disconnect: Why Wall Street is Mispricing ACADIA's $1 Billion Transformation

ACADIA's stock is mispriced. It's a profitable $1B+ revenue company with $820M cash, yet trades low due to misunderstood tax-related insider sales and temporary IRA charges. The market ignores its strong financials and pipeline.

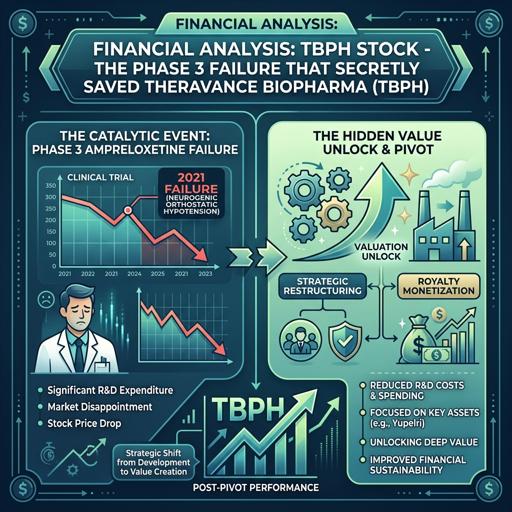

The Phase 3 Failure That Secretly Saved Theravance Biopharma (TBPH)

Theravance Biopharma's stock crashed after a Phase 3 trial failure. However, the company now has a strong cash position, zero debt, and profitable assets like YUPELRI and Trelegy royalties. With R&D costs slashed, it's transitioning to a cash-generating business at a deeply undervalued price.

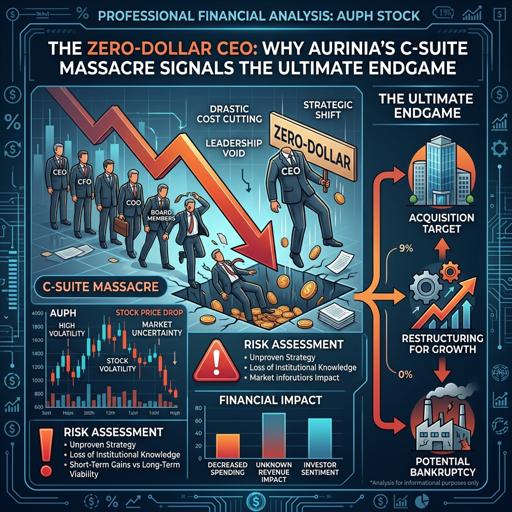

The Zero-Dollar CEO: Why Aurinia’s C-Suite Massacre Signals the Ultimate Endgame

Aurinia's stock surge is just the start. The biotech is now a cash-generating machine with a cheap valuation. A recent boardroom coup by activist Kevin Tang signals a likely sale or major strategic shift is imminent.

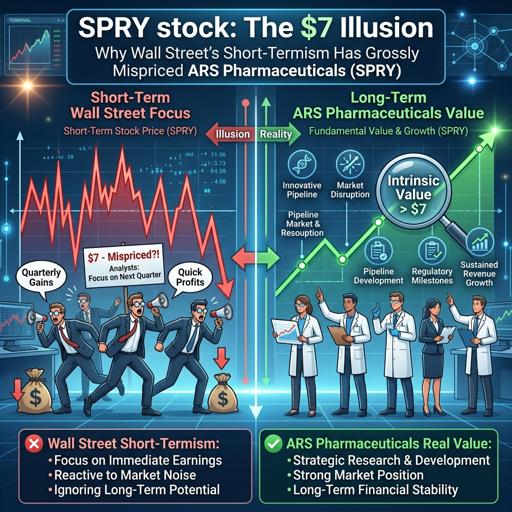

The $7 Illusion: Why Wall Street's Short-Termism Has Grossly Mispriced ARS Pharmaceuticals (SPRY)

Wall Street's short-term focus has mispriced ARS Pharmaceuticals (SPRY). The market is fixated on launch losses, ignoring its strong revenue start, ample cash, and potential to disrupt the multi-billion dollar epinephrine market.

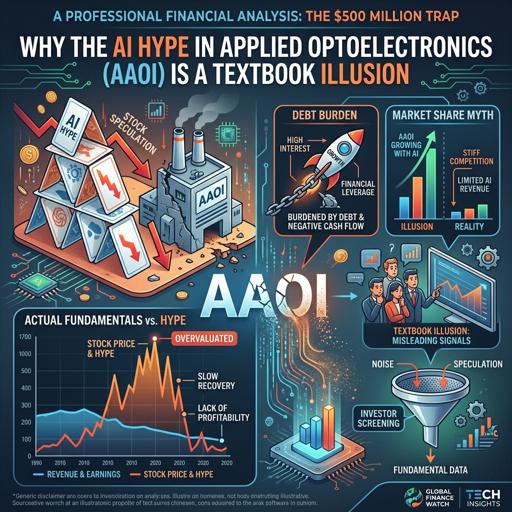

The $500 Million Trap: Why the AI Hype in Applied Optoelectronics (AAOI) is a Textbook Illusion

AAOI's stock surged on AI hype, hitting a $6.5B valuation. However, the company is still losing money despite record revenue, and insiders are aggressively selling their shares.

Priced for Perfection: The $6.5 Billion Question Hanging Over Apogee Therapeutics

Apogee's stock soared 96% on strong trial data, valuing it at $6.5B. However, insiders are aggressively selling shares, signaling major risk for the pre-revenue biotech.

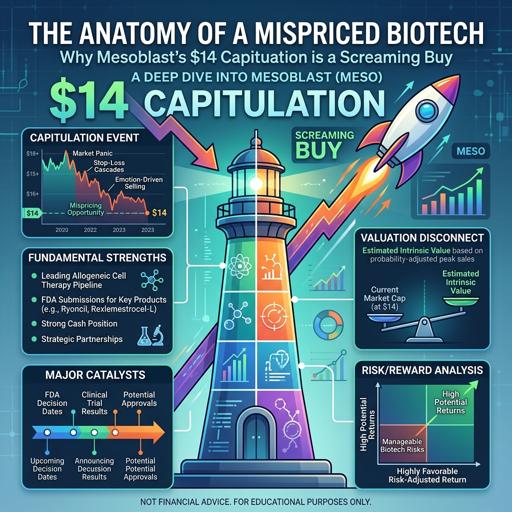

The Anatomy of a Mispriced Biotech: Why Mesoblast’s $14 Capitulation is a Screaming Buy

Mesoblast's $14 stock price is a mispriced opportunity. A key insider bought out toxic debt, provided cheap financing, and invested $16M in shares. The company is now commercial with strong revenue growth, not a speculative cash burn.

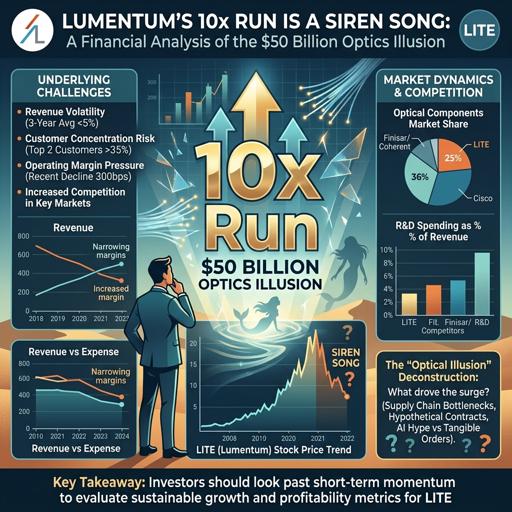

The $50 Billion Optics Illusion: Why Lumentum's 10x Run is a Siren Song

Lumentum's $50B valuation is inflated by NVIDIA's strategic investment. The deal secures NVIDIA's supply chain, not Lumentum's pricing power. Insiders are selling, signaling the stock's AI optics hype is unsustainable.

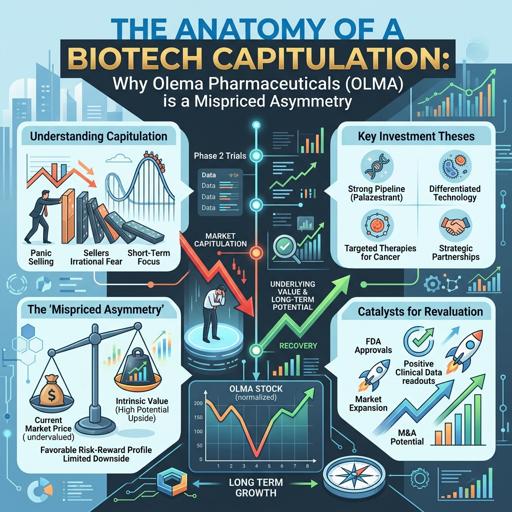

The Anatomy of a Biotech Capitulation: Why Olema Pharmaceuticals (OLMA) is a Mispriced Asymmetry

Olema Pharmaceuticals (OLMA) stock fell 60% on retail panic over insider sales and a CFO departure. However, sophisticated institutions like Fidelity doubled their stakes, buying heavily into the selloff. The company's fundamentals remain strong with a solid cash position.

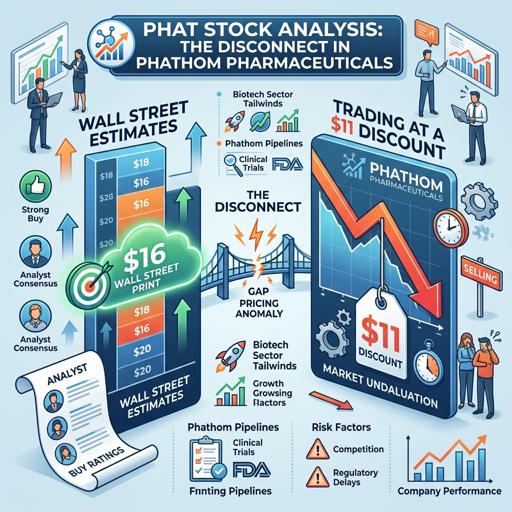

The Disconnect in Phathom Pharmaceuticals: A $16 Wall Street Print Now Trading at an $11 Discount

Phathom stock trades at $11.21, a 30% discount to its $16 January offering price. Despite technical weakness, the firm shows explosive 217% revenue growth and a path to profitability in 2026.

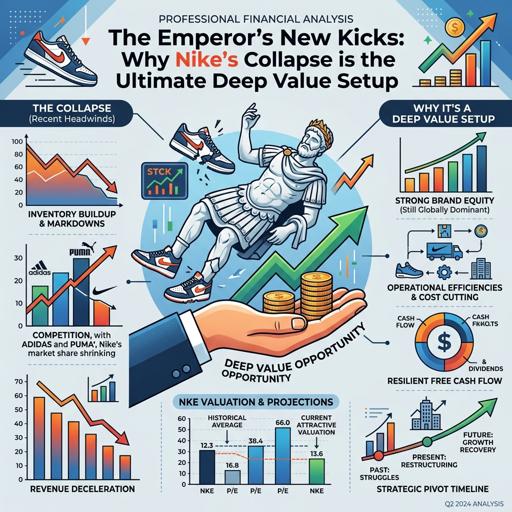

The Emperor's New Kicks: Why Nike's Collapse is the Ultimate Deep Value Setup

Nike's stock collapse is a contrarian deep value setup. The company is undergoing a necessary operational reset, re-engaging wholesale partners to clear inventory and restructuring its leadership for efficiency.

Sarepta Therapeutics (SRPT): An Investment Analysis at the Precipice of Crisis and Opportunity

Sarepta Therapeutics, a leader in precision genetic medicine, faces an existential crisis in 2025 due to patient deaths linked to its flagship gene therapy, ELEVIDYS, triggering severe FDA regulatory actions and a sharp market decline. Despite this, the company maintains a durable revenue base from its RNA-based PMO therapies, which accounted for 54% of 2024 net product revenue. Financially, Sarepta reported record Q2 2025 results, but its valuation has collapsed, pricing in worst-case scenarios. In response, management has initiated restructuring, preserved capital, and pivoted strategically through a partnership with Arrowhead Pharmaceuticals to access siRNA technology. The investment thesis presents a high-risk, binary opportunity: potential multi-fold returns if ELEVIDYS is salvaged and the new platform succeeds, versus significant capital loss if regulatory and safety issues prove insurmountable. This speculative proposition is suited only for risk-tolerant, long-term investors.

An Investment Analysis of Trevi Therapeutics, Inc. (TRVI)

Trevi Therapeutics (TRVI) is a clinical-stage biopharmaceutical company focused on developing its sole asset, Haduvio (oral nalbuphine ER), as a first-in-class treatment for chronic cough in Idiopathic Pulmonary Fibrosis (IPF) and Refractory Chronic Cough (RCC)—conditions with no approved therapies in the U.S. The drug demonstrated strong efficacy in Phase 2 trials (CORAL for IPF and RIVER for RCC), showing significant cough reduction and a manageable safety profile. With a cash runway extending into 2029 following a recent $115 million financing, the company is well-positioned to advance into Phase 3 trials starting in H1 2026. Despite promising clinical and financial de-risking, investment carries significant risks due to its single-asset focus, potential Phase 3 failure, and commercialization challenges. A "Buy" recommendation is advised for high-risk, long-term investors, given the asymmetric upside potential.

An In-Depth Analysis of Larimar Therapeutics (NASDAQ: LRMR): A High-Risk, High-Reward Venture into Friedreich's Ataxia

Larimar Therapeutics is a clinical-stage biotech company focused on developing nomlabofusp (CTI-1601), a protein replacement therapy for Friedreich's ataxia (FA), a rare neurodegenerative disease. The investment thesis presents a high-risk, high-reward opportunity centered on this single asset. The bull case highlights nomlabofusp's unique mechanism targeting the root cause of FA by restoring frataxin levels, supported by promising Phase 1/2 data showing dose-dependent increases in frataxin. Regulatory de-risking, including the FDA's removal of a clinical hold and acceptance of frataxin as a surrogate endpoint, strengthens the path to potential accelerated approval. However, significant risks persist: Larimar is pre-revenue with a tight cash runway into late 2026, faces competition from Biogen's approved therapy SKYCLARYS, and relies on upcoming clinical data readouts. The recommendation is a speculative buy for risk-tolerant investors, emphasizing the potential for substantial returns if successful but acknowledging the possibility of total capital loss.

KALA BIO (NASDAQ: KALA): An In-Depth Analysis of a High-Stakes Clinical Catalyst in Rare Ophthalmic Disease

KALA BIO, Inc. (NASDAQ: KALA) is a clinical-stage biopharmaceutical company whose investment potential hinges entirely on the success of its lead candidate, KPI-012, for treating Persistent Corneal Epithelial Defect (PCED). The company has strategically repositioned itself as a pure R&D entity after divesting its commercial assets, focusing all resources on its Mesenchymal Stem Cell Secretome (MSC-S) platform. The critical catalyst is the topline data from the Phase 2b CHASE trial, expected by the end of September 2025. A positive outcome could validate the platform and unlock a significant market with no approved therapies, while failure would severely impact the company's valuation. Financially, KALA is pre-revenue with a history of losses and shareholder dilution. Despite sufficient cash to fund operations into Q1 2026, a successful trial would necessitate immediate capital raising for further development. The investment is rated as a Speculative Buy, suitable only for high-risk investors aligned with the binary nature of the upcoming clinical results.

GigaCloud Technology Inc. (GCT): An Analysis of a Deeply Undervalued E-commerce Disruptor with Elevated Risks

GigaCloud Technology Inc. (GCT) presents a compelling but high-risk investment opportunity. The company operates an innovative B2B e-commerce platform specializing in large-parcel goods, utilizing its proprietary Supplier Fulfilled Retailing® model to streamline logistics. It demonstrates strong financials with consistent revenue growth, high profitability, and a debt-free balance sheet supported by significant cash reserves. However, the stock trades at a steep valuation discount due to serious short-seller allegations of fraudulent activities and substantial geopolitical exposure tied to its reliance on Chinese manufacturing. Given these binary risks, the analysis recommends a Speculative Buy for risk-tolerant, long-term investors, as a resolution in the company’s favor could trigger significant valuation upside.

An In-Depth Investment Analysis of Invivyd, Inc. (NASDAQ: IVVD): A High-Stakes Play on the Future of Infectious Disease Prevention

Invivyd, Inc. (IVVD) represents a high-risk, high-reward investment opportunity centered on its next-generation monoclonal antibody, VYD2311, which has secured an accelerated FDA approval pathway. While the company’s proprietary INVYMAB™ platform shows scientific promise for rapidly addressing viral evolution, it faces severe financial challenges, including a high cash burn rate, recent dilutive financing, and significant institutional divestment. Revenue from its commercialized product, PEMGARDA®, remains insufficient to ensure sustainability. The investment thesis is binary: success of VYD2311 could drive substantial valuation upside, while clinical or regulatory failure poses existential risk. Recommended only for risk-tolerant investors with capacity for potential total loss, active monitoring of key catalysts is essential.